Good Credit Pays More?

New Government Guidelines create Confusion

There has been a lot of confusion and frustration in the news lately regarding the new mortgage fees. As a former banker with expertise in mortgage pricing and as an economist that researchers housing markets, I wanted to provide you with some clarification on the topic.

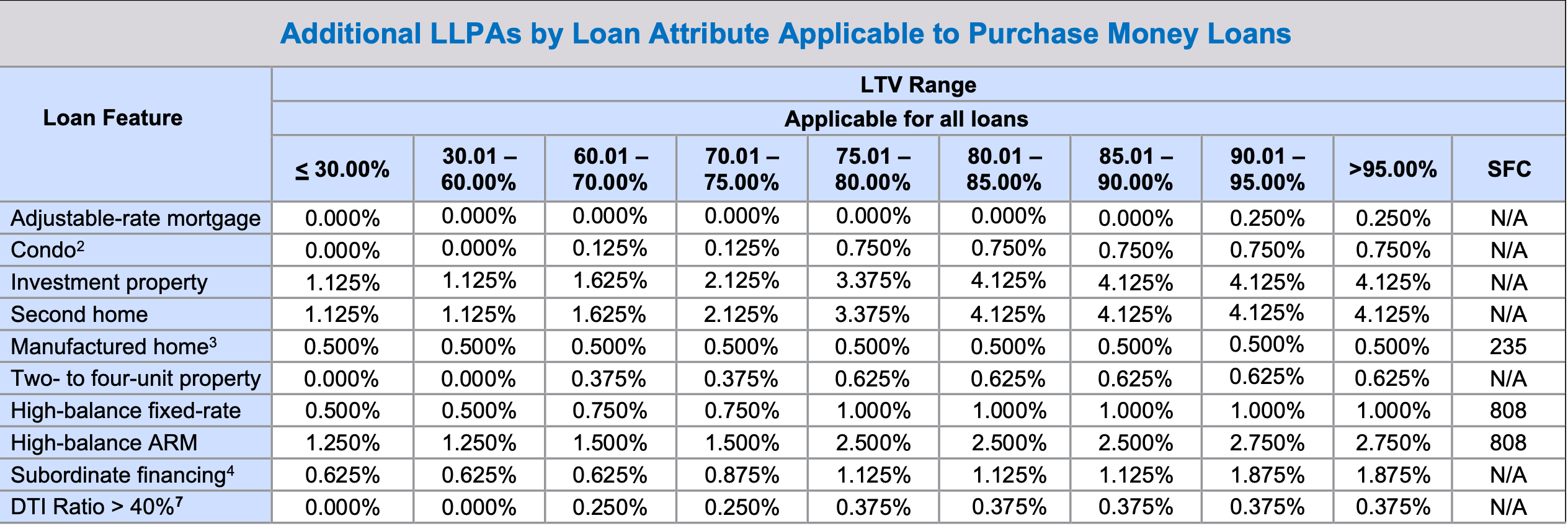

First, it is important to understand how mortgage pricing works. For conforming loans, which account for 85% of all loans in 2021, there is a base interest rate that fluctuates with the market. The lender then makes modifications to the interest rate based on additional risk factors of the borrower, such as property type, loan-to-value ratio, credit score, and possibly many more risk adjustments.

There have been some news headlines suggesting that the new mortgage pricing causes people with good credit scores to pay more for mortgages than those with bad credit scores. This is not correct. The credit score adjustment shows that individuals with better credit always pay less of a risk premium compared to individuals with lower credit scores, meaning that good credit score individuals still pay a lower risk premium than low credit score individuals.

The confusion stems from mistaking changes with levels. What others are doing is comparing the risk premium for high credit scores before and after May 1, then comparing that to the change in premiums for low credit scores. In that case, what has happened is good credit score risk premium has increased, and low credit score risk premium has decreased. And this confused the market and generated the language that high credit score individuals are being penalized and that took over the news. The reality is these adjustments happen all the time and depends on risk changes and portfolio considerations.

While I am not here to discuss if this policy is good or bad, I wanted to clarify what is going on and how to better understand the new government guidelines. It is also important to note that the lender has more discretion to add and subtract from the interest rate based on their portfolio needs and customer negotiation skills.

I hope this information has been helpful in clarifying the confusion surrounding the new mortgage fees. If you have any questions or comments, please leave them below. Also, please like and share this newsletter to help me reach more people.

Here is this weeks video with an example and something you can share with anyone that would benefit.

Research Corner

Interested in learning more about my research in this area? Checkout the following paper on mortgage pricing and bank competition.

Al-Bahrani, A. (2016). Competition in Online Markets: When Banks Compete, Do Consumers Really Win?. Journal of Housing Research, 25(2), 157-170.