Why Making Financial Decisions is Hard!

Building our community together

As we step into April and celebrate Financial Literacy Month, we plan to dig deeper into personal finance and economic decision-making complexities. This year, we start our discussion by paying homage to the groundbreaking work of Daniel Kahneman, a seminal figure in the field of behavioral economics who recently passed away.

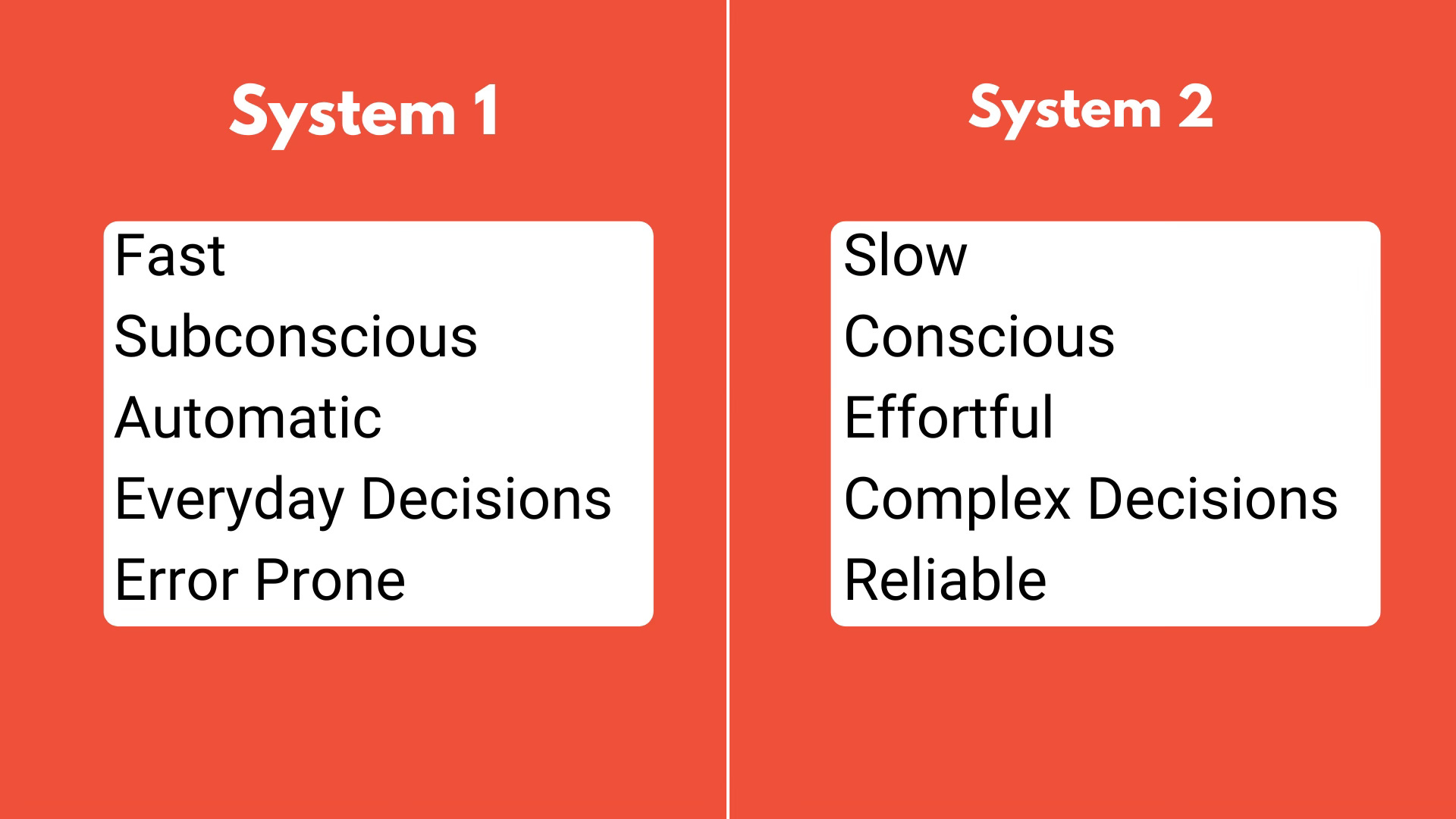

Kahneman's research, notably encapsulated in his bestselling book, "Thinking, Fast and Slow," has fundamentally altered our understanding of how humans make economic decisions. He introduced us to the concepts of "System 1" and "System 2" thinking, illustrating how our quick, intuitive reactions (System 1) often clash with our slower, more deliberate thought processes (System 2). This framework isn’t just for academic discussion; a good understanding of our decision-making process allows us to confront our financial behaviors more critically.

In honoring Kahneman's legacy, we focus on the essence of behavioral personal finance. This field merges the insights of behavioral economics with the difficulties of managing money. Behavioral economics highlights that humans aren’t rational, and their decisions often go against their long-term goals.

System Failures

Relying predominantly on System 1 for financial decisions often results in choices that seem easier or more comfortable at the moment but may not serve our long-term interests. Reflecting on my own experiences, the challenge of saving for retirement stands out. Despite understanding its importance, I struggled to prioritize it early in my career. This was a textbook example of System 1's influence: focusing on immediate needs and gratifications overshadowed the critical goal of securing my future.

My approach to managing financial decisions contributed to these challenges. Instead of setting aside specific times for financial planning, I attempted to fit these decisions into my existing schedule, often relegating them to the end of the day. This timing made me susceptible to ego depletion—a state where mental fatigue diminishes our capacity for critical thinking and complex decision-making. In these moments, drained from the day's demands, I found myself either too exhausted to engage in thorough analysis or overwhelmed by the complexity of the decisions. Consequently, I often opted for the most straightforward route, mistaking it for the path of least resistance when, in fact, it was a shortcut to suboptimal outcomes.

The lesson from these experiences is clear: financial decision-making demands our full attention and a strategic approach. By recognizing System 1's limitations and the impact of ego depletion, we can better navigate the intricacies of personal finance, making choices that align with our long-term aspirations rather than the fleeting comforts of the present.

Create a System

In light of Kahneman's insights into human decision-making, establishing a structured approach to your finances is critical. One of the changes that I made was automating my decisions. By automating my savings, I ensure a consistent commitment to my financial goals and mitigate the risk of succumbing to the temptation of immediate gratification. Similarly, I set one day a month for financial planning and goal setting. Crafting a clear, actionable plan for my investments and debt repayment provides direction and control, steering me away from the pitfalls of indecision and the overwhelming nature of unstructured financial management.

This systematic approach to personal finance does more than streamline financial activities; it addresses the psychological barriers to effective money management. Without a plan, our biases often fill the void. Conversely, a well-defined system transforms your budget from a source of stress into a manageable, even empowering, aspect of your life.

Takeaways

Understand Your Biases: Acknowledge that biases like overconfidence and loss aversion can skew your financial decisions. Recognizing these can be the first step towards more rational financial planning and investment choices.

Set Clear Financial Goals: Kahneman’s work underscores the importance of clarity in goal-setting. Whether saving for retirement, buying a home, or building an emergency fund, clear goals can help guide your financial decisions and reduce impulsive behaviors. I have found that having a tangible reason to save keeps me committed and excited about the future.

Create a Financial Plan: A well-structured plan is a roadmap for your financial journey. It can help you allocate resources efficiently and prepare for opportunities and challenges. By creating a plan, you avoid making daily financial decisions and falling victim to ego depletion.

Embrace Patience and Discipline: Kahneman’s advocacy for slow, deliberate thinking in financial decision-making is a testament to the power of patience and discipline. In an era of instant gratification, this is more crucial than ever. When talking to my students, I often remind them that wealth accumulation takes time. If you expect quick returns or immediate results, you will be disappointed.

Continuous Education: Commit to lifelong learning. The financial landscape constantly evolves, and staying informed is essential to navigate it successfully. Resources like books, podcasts, and seminars can be invaluable.

April Giveaway

April is financial literacy month. To celebrate, we are creating a series of content designed to answer any financial literacy questions or concerns you might have. We would love your help in collecting questions.

Completing the form and providing your name and email allows you to qualify for a copy of The Psychology of Money.

Here's to making informed and thoughtful financial decisions.

The fine print: The winner will be randomly selected on April 19th. You must provide your email address so we can contact you, and you must be located in the United States.

I'm intrigued by the idea of "ego depletion." I also find that I put off the most overwhelming (yet often most important) decisions until the last minute.

I’m 2/3 of the way through Thinking Fast and Slow and I’ve probably recommended it to 10 people. Phenomenal book.